What’s the best pension for property investors?

In recent years there has been an explosion of financial products available to investors. This has resulted in increased flexibility and choice. Today’s investors have the luxury of being able to make money in rising and falling markets, as well as having the ability to take advantage of various tax reliefs. However, as a property investment company, we are often asked, what is the best pension for property investors? In this article, we will show you how to have your preverbal cake and eat it concerning property investing.

What is better property or a pension?

This subject was covered extensively in a previous article titled, is property better than a pension? We concluded that for most people a pension edged it. This is due to the preferential tax benefits given for pension investing. Though for some investors, the answer is not so clear cut, due to the ability to use mortgage finance to magnify investment returns. To recap the pros and cons of pension investing is listed in the table below.

Pension investing

| Advantages of pension investing | Disadvantages of pension investing |

| Your employer is expected to contribute | Potential shortfall |

| Your employer may match your contributions | Volatility |

| You can get a tax credit for extra money you pay into a pension | Fees |

| Tax-free lump sum | Complexity |

| The power of compounding | No leverage |

| You could opt for a staged drawdown or a combination of drawdown and annuity | Money is tied in |

| Volatility can be your friend | More conservative returns in final years to reduce risk of losses |

Property investing

In contrast, investing into property instead of a pension has its advantages and disadvantages as well. Below we highlight the key pros and cons.

| Advantages of property investing | Disadvantages of property investing |

| Mortgage finance allows increased returns | Fewer tax benefits – no tax credit for investing |

| Self-financing portfolio as property appreciates | Stamp duty – Buy-to-let surcharge |

| Rental income | Changes to mortgage interest rate relief |

| Emerging models for better returns eg vacation rentals & HMOs | Professional fees – solicitors, mortgage brokers, accountants, maintenance et |

| Flexibility – you can sell your property at any time | Hassle – Conveyancing, lettings and maintenance |

| Legacy – property can be passed down | Void periods and problem tenants |

| Performance – UK property has outperformed UK equities in recent years | Selling costs – CGT and restate agents fees |

Overall

Whilst there are lots of pros and cons for both pensions and property. The key benefit on pension investing is tax relief. For 40% tax payers the net effect of investing in a pension is only having to pay 60 pence for each pound in a pension. This allows an investor to have a bigger pot which will start compounding.

The key benefit of property investing is the ability to use mortgage finance to multiply investment gains. Furthermore, as a property appreciates an investor can refinance to release further equity which can be used to buy additional property to further magnify returns.

SIPP versus SSAS

Investing in property through a pension

For UK investors there are two types of pension funds which permit investing in property. These are Small Self-Administered Schemes (SSAS) and a Self-Invested Personal Pension. The former might me more suitable for business owners, whilst non business owners can only invest directly in property through a SIPP.

Neither schemes permit investing in primarily residential property without having a large tax penalty. Therefore, both schemes need to buy commercial property. Though investing in a shop with a flat above is permitted providing you rent the flat out instead of you or an employee living in it.

Below we outline the key differences between these two schemes.

Differences between a SSAS and a SIPP

In reality both these schemes have a lot in common though there are some key diffences.

Key differences

SIPP:

- open to anyone

- can’t lend to the company

- type of personal pension – higher running costs

- SIPP provider acts as the trustee

SSAS:

- greater investment flexibility and control

- can lend to the company

- members are usually trustees

- usually only available to company directors

Both schemes are regulated in the same way in the eyes of HM Revenue and Customs (HMRC). They are both investment regulated pension schemes. This means that the basic rules surrounding borrowing, lending and investment are identical.

However, whilst the underlying tax rules are the same, the legislation is applied slightly differently.

So what’s the difference?

Below we outline the differences between a SIPP and a SASS with respect to governance and eligibility.

SIPP

A SIPP is a personal pension plan set up by an insurance company or specialist SIPP operator where the member has greater control over the investments. A SIPP is open to anyone (assuming they meet the provider’s eligibility requirements). The key features include:

- It is a personal pension plan.

- The option to invest in both non-insured assets such as unit trusts and property and insured assets such as a trustee investment plan.

- A member’s employer can contribute to the pension plan.

SSAS

A SSAS is a small occupational pension scheme that is set up by the directors of a business. A SASS allows for more control over the investment decisions relating to their pensions. Importantly, a SASS allows the directors to use the pension to invest in the business. Because of this, each member of the SSAS is usually a trustee.

The following are features of a SSAS:

- It is an occupational pension scheme.

- The members are usually employees or directors of the sponsoring employer.

- These schemes tend to be relatively small.

- Each member has a notional share of the SSAS funds. This includes non-insured assets such as property and possibly insured money held in a trustee investment plan.

Investment

A SSAS has more flexibility than a SIPP when it comes to investment, as current legislation allows investments to be made in the sponsoring employer. A SIPP doesn’t have a sponsoring employer but a SSAS does. This is why a SSAS can invest in the company.

Below we list the key investment differences between each scheme.

| SSAS | SIPP |

|---|---|

| SSAS can lend money to sponsoring employers. | Loans are not allowed to any members or any person/company connected to the member. Any such loan made by a SIPP would be an unauthorised payment. |

| Can invest up to 5% of the fund value in the shares of the sponsoring company. | A SIPP doesn’t have a sponsoring employer so can theoretically invest up to 100% of the fund in the shares of any company. However if it’s a company owned or controlled by the member, that’s regarded as investing in taxable property. |

| Can buy shares in more than one sponsoring employer so long as the total market value at the time the shares are bought is less than 20% of the total value of the scheme. | If the company involved is controlled by the SIPP member or an associated person, investment in that company would be regarded as investing in taxable property. |

| SSAS can potentially own 100% of a company’s shares so long as the value doesn’t exceed 5% of the value of the SSAS. | A SIPP can potentially own 100% of a company’s shares so long as the company is not controlled by the member, and this is acceptable to the SIPP provider. |

Which is the best pension for property investors?

As you can see, a SASS is only available to company owners. If this applies to you then it is something you may wish to consider. The key benefit of a SASS is you can invest your employees pension into your own commercial property which is of a great benefit to the company. On the flip side there is more responsibility and red tap to deal with should you opt to go down this route.

At Esper Wealth we work alongside fully regulated investment professionals who can assist you with setting up a SASS or a SIPP. If this is of interest to you then you should contact your account manager who will schedule you an appointment with a pension specialist.

Are there other options?

Yes, and no. These two schemes are the only way to directly invest in property through a pension. However there are lots of indirect methods. A previous article titled, how to invest in property through a pension explains your options in greater detail. Though we highlight your main options below.

OEICs and Unit Trusts

Several collective investment schemes that invest exclusively in property. Whilst you are not owning property directly, you can invest in these schemes through your pension.

REITs

Real Estate Investment Trusts are investment trusts that invest in property. These schemes have the additional benefit that the company is exempt from corporation tax. This makes REITs a very tax-efficient way of investing in property through your pension.

Shares

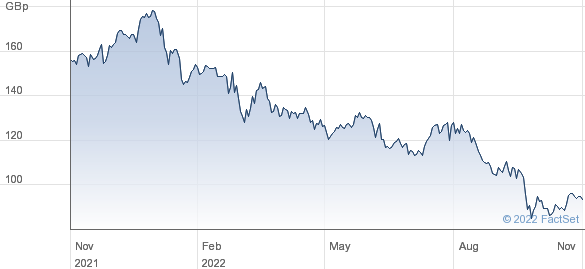

It is possible to invest directly in shares through your pension. Many investors opt for national housebuilders. Currently, these have depressed share prices. This represents a good buying opportunity for long term investment.

Bonds

Property Bonds are another way to invest in property through your pension. By selecting this investment type you will get a fixed income in the form of a dividend. Interestingly, as interest rates are rising, the capital value of listed bonds is going down. This is due to the inverse relationship between bond prices and interest rates. This is because as rates rise you can get higher rates on your savings. So yields on bonds become less attractive. It is expected that interest rates will peak at the tail end of 2023 so this would be the best time to buy property bonds. As when interest rates start to fall the capital value of bonds will rise. For an investor, this means gaining capital growth in addition to your fixed income.

Investment Review

At Esper Wealth we offer a consultative approach to investing. As part of our service, we offer all prospective clients a free investment review. An investment review is our opportunity to get to know you better, to understand your needs, wants and attitude to risk. This will help us to identify the investment products that are most suited to you. Perhaps, just as importantly we can advice you on the products to avoid as they are not suited to your specific needs.

If you would like to take advantage of this free service then contact us today and we will schedule you an appointment with one of our experienced advisors.